Visa Claims Resolution (VCR) is Visa’s current guidance for managing payment disputes — traditionally referred to as chargebacks. VCR replaced Visa’s legacy chargeback process in 2018.

VCR was created to simplify workflows and resolve disputes quicker.

While revamping the card brand’s processes, VCR introduced several new elements.

- New terms were introduced and definitions for certain existing terms changed.

- Visa pivoted from one workflow to two — adding the allocation workflow to the existing collaboration workflow.

- Reason codes were reformatted and put into groups. Codes that start with 10 are considered fraud, codes that start with 11 are authorisation disputes, codes that start with 12 are processing errors, and codes that start with 13 are consumer disputes.

- Chargeback time limits were reduced. Many issuer time limits were dropped from 120 days to 75 days, while acquirer time limits went from 45 days to 30 days.

Let’s take a look at each new element individually.

Key Terminology

Visa uses its own terminology for certain words that differ from other card brands. Here are key terms to know.

- Transaction Inquiry – A transaction inquiry is a formal request that an issuer makes to Visa to obtain information about the transaction that is being challenged. This process is typically initiated after a cardholder raises a dispute.

- Associated Transactions – Visa responds to a transaction inquiry with a list of associated transactions (previous credits, reversals, adjustments, etc.) that could proactively make the dispute invalid.

- Allocation – Allocation is a workflow that allows Visa to use internal data and automation to assign responsibility for a dispute.

- Collaboration – Collaboration is a litigation-based dispute resolution process.

- Dispute – Instead of using the word chargeback, Visa uses the term dispute.

- Dispute Condition – Dispute conditions — called reason codes by other brands — explain why cardholders dispute transactions. When VCR was unveiled, Visa replaced 22 reason codes with 24 dispute conditions.

- Dispute Category – Visa categorizes the dispute conditions as fraud, authorization, processing error, and consumer disputes.

- Dispute Response – A dispute response is the formal evidence and documentation a merchant uses to contest a dispute. Visa replaced the word representment with dispute response.

- Pre-Arbitration – During the allocation process, liability is automatically assigned, so merchants don’t have the opportunity for a dispute response. However, merchants can respond via pre-arbitration to share compelling evidence and argue their side of the case.

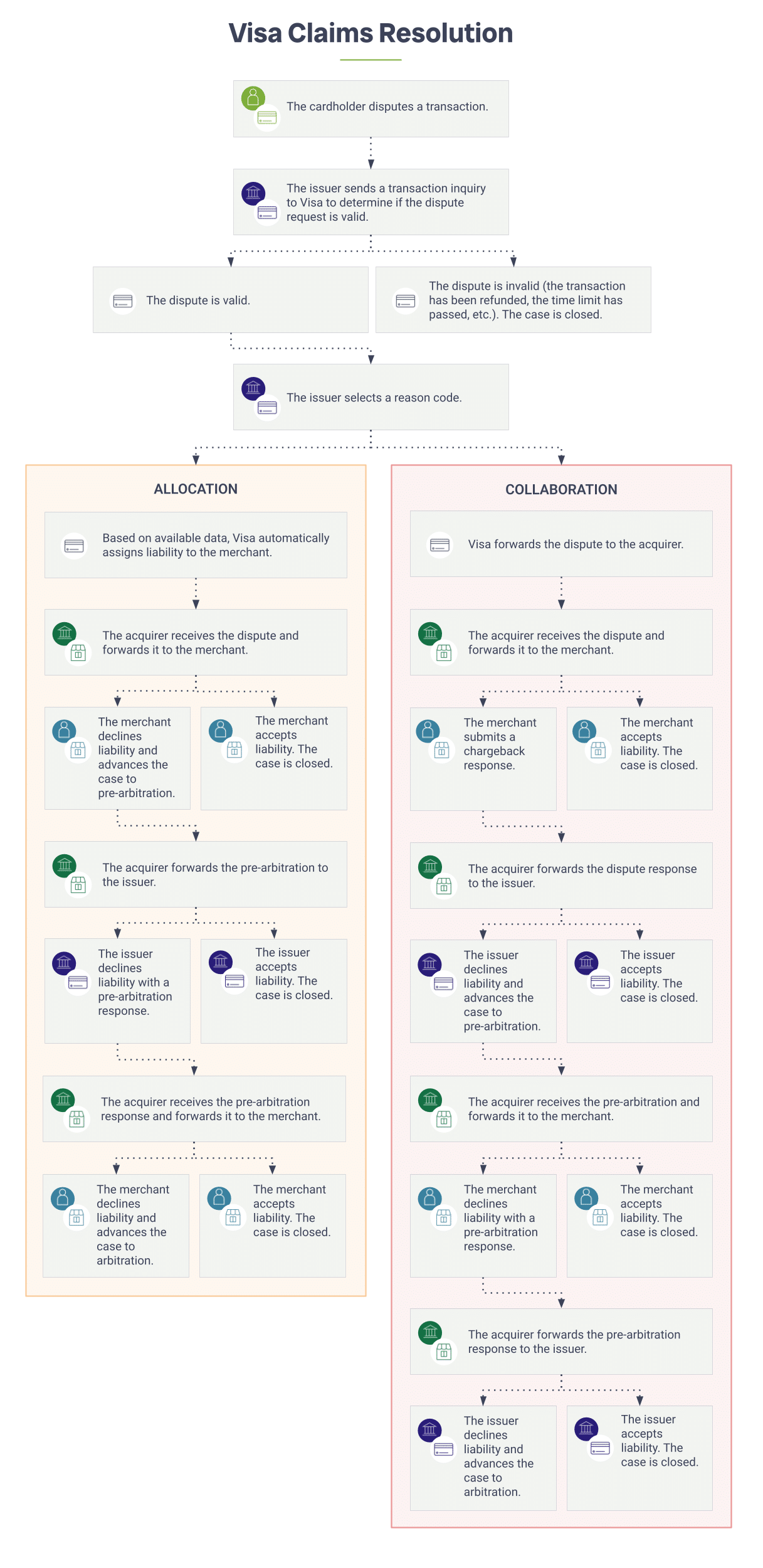

Dispute Resolution Processes: Allocation vs. Collaboration

VCR features two distinct dispute resolution styles: allocation and collaboration.

- Allocation uses Visa’s internal data to automatically assign liability to either the cardholder or merchant.

- Collaboration is a litigation-based workflow that allows the issuer and acquirer to both present their side of the story before liability is assigned.

Here’s an overview of the two paths a dispute could take.

Check our related glossary entries to learn more about each workflow:

Visa Reason Codes

The VCR initiative updated Visa’s dispute conditions (commonly referred to as reason codes).

The reason codes are divided into four categories:

Fraud

- 10.1 – EMV Liability Shift Counterfeit Fraud

- 10.2 – EMV Liability Shift Non-Counterfeit Fraud

- 10.3 – Other Fraud – Card-Present Environment

- 10.4 – Other Fraud – Card-Absent Environment

- 10.5 – Visa Fraud Monitoring Program

Authorization

- 11.1 – Card Recovery Bulletin

- 11.2 – Declined Authorization

- 11.3 – No Authorization/Late Presentment

Processing Errors

- 12.2 – Incorrect Transaction Code

- 12.3 – Incorrect Currency

- 12.4 – Incorrect Account Number

- 12.5 – Incorrect Amount

- 12.6 – Duplicate Processing/Paid by Other Means

- 12.7 – Invalid Data

Cardholder Dispute

- 13.1 – Merchandise/Services Not Received

- 13.2 – Cancelled Recurring Transaction

- 13.3 – Not as Described or Defective Merchandise/Services

- 13.4 – Counterfeit Merchandise

- 13.5 – Misrepresentation

- 13.6 – Credit Not Processed

- 13.7 – Cancelled Merchandise/Services

- 13.8 – Original Credit Transaction Not Accepted

- 13.9 – Non-Receipt of Cash at an ATM

Visa Chargeback Time Limits

VCR adjusted the timelines for chargebacks. Here’s a high-level overview. Visit our chargeback time limits glossary entry to learn more.

Allocation disputes

- Issuer time limit to file a chargeback: 120 days (fraud disputes) or 75 days (authorization disputes) from the transaction processing date

- Acquirer time limit to file pre-arbitration attempt: 30 days from the chargeback filing date

- Issuer time limit to file a pre-arbitration response: 30 days from the pre-arbitration attempt

- Acquirer time limit to file arbitration: 10 days from the pre-arbitration response filing date

Collaboration disputes

- Issuer time limit to file a chargeback: 120 days from the transaction processing date

- Acquirer time limit to file a chargeback response: 30 days from the chargeback filing date

- Issuer time limit to file a pre-arbitration attempt: 30 days from the chargeback filing date

- Acquirer time limit to file a pre-arbitration response: 30 days from the pre-arbitration attempt

- Issuer time limit to file arbitration: 10 days from the pre-arbitration response filing date