Allocation is a chargeback management workflow introduced by Visa during the 2018 Visa Claims Resolution (VCR) initiative.

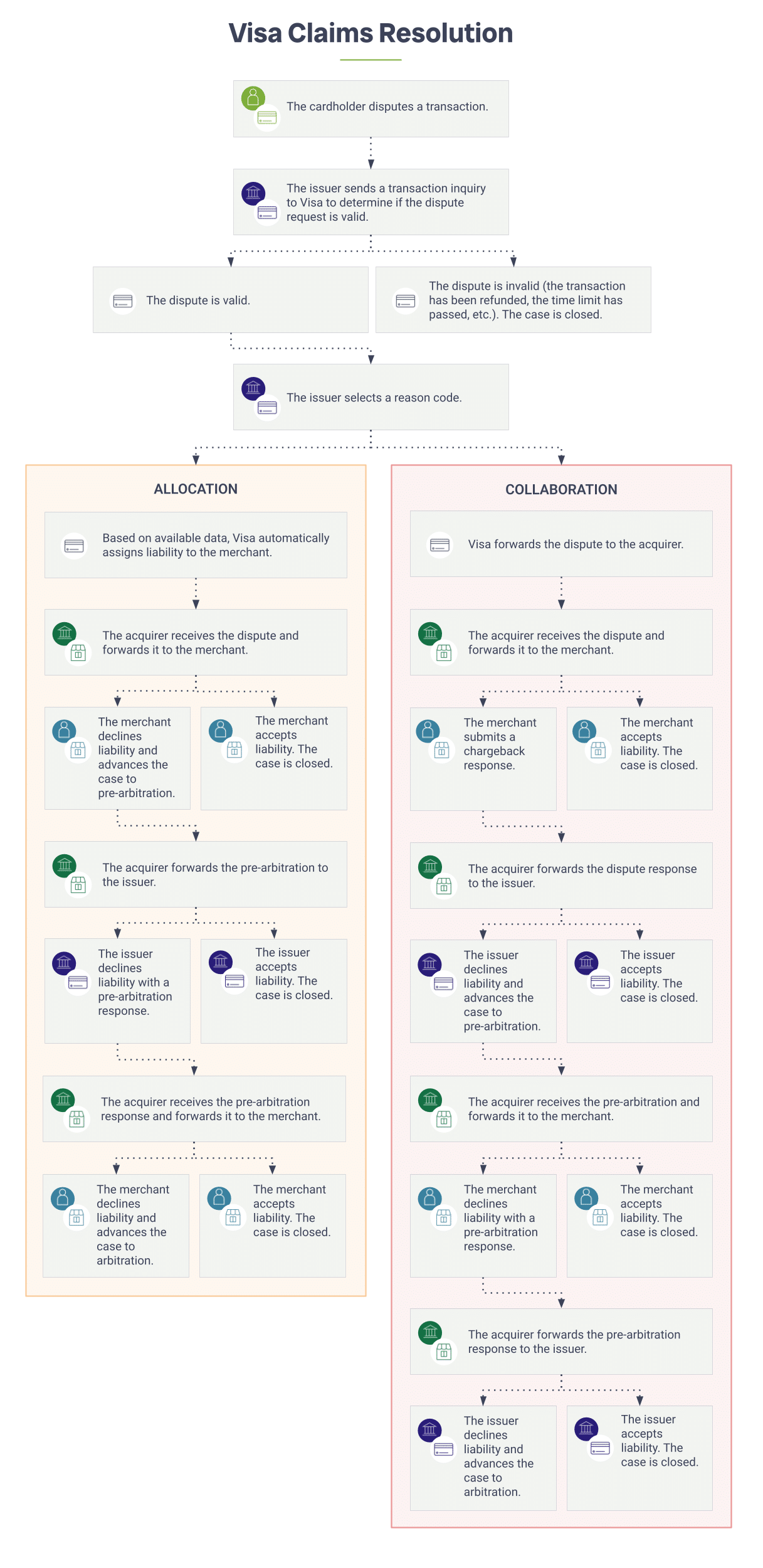

With VCR , Visa pivoted from one workflow to two: allocation and collaboration.

Allocation uses Visa’s internal data to automatically assign liability to either the issuer or acquirer. Collaboration, on the other hand, is a litigation-style workflow that allows the issuer and acquirer to debate liability.

Allocation is used to manage chargebacks that fall into the fraud category (dispute reason codes that start with 10) and the authorization issues category (dispute reason codes that start with 11).

Unlike collaboration — and the chargeback process used by other card brands — allocation only uses four of the five dispute resolution phases.

- Chargeback

- Pre-arbitration

- Pre-arbitration response

- Arbitration

If liability is assigned to the issuer, the case is closed and the bank or cardholder is responsible for paying the transaction.

The following are examples of what might cause Visa to automatically assign liability to the issuer.

- The chargeback time limit has passed.

- The issuer approved the transaction via the authorization process.

- The transaction was fully authenticated by Visa Secure with 3D Secure.

If liability for the dispute is assigned to the merchant via the acquirer, the merchant can either accept responsibility or respond.

The following are examples of what might cause Visa to automatically assign liability to the acquirer:

- The cardholder has a chip-enabled EMV card, but the merchant swiped the card.

- The merchant didn’t request authorization, so a stolen card was used without permission.

- The merchant didn’t settle the transaction within the acceptable time limit.

However, because liability has already been assessed for allocation disputes, there technically isn’t a dispute response opportunity for merchants. Instead, the response is considered pre-arbitration.

And pre-arbitration is typically only applicable if the merchant has information that wasn’t accessible by Visa in the decision-making process. For example, in response to a fraud claim, photos or emails that prove a link between the cardholder and the person receiving the merchandise or services.

If the dispute isn’t resolved during the pre-arbitration phase, the case can advance to arbitration if necessary.

Because one of the dispute process stages is removed, issuer and acquirer filing responsibilities differ from the collaboration workflow. Here’s an overview.

| Workflow stage | Collaboration | Allocation |

|---|---|---|

| Chargeback | Initiated by the issuer | Initiated by the issuer |

| Chargeback response | Initiated by the acquirer | Omitted |

| Pre-arbitration | Initiated by the issuer | Initiated by the acquirer |

| Pre-arbitration response | Initiated by the acquirer | Initiated by the issuer |

| Arbitration | Initiated by the issuer | Initiated by the acquirer |

AltoPay aims to simplify the complexities of payments — including chargeback management. Regardless of which path a dispute takes — allocation or collaboration — we can help you manage it with our chargeback management solutions.

Allocation vs. Collaboration

Both Visa workflows give you, the merchant, the opportunity to challenge invalid disputes and recover revenue that has been unfairly sacrificed. However, the way you go about doing that differs.

When Visa launched the VCR initiative, the brand’s goal was to simplify the dispute process and increase efficiency. As you can see, the allocation process is much shorter — with less back-and-forth — than collaboration.