An authorization hold is a temporary hold that freezes a cardholder’s funds or credit. It takes effect after a transaction has been approved and lasts until the transaction is finalized (settled). Funds are reserved by the card issuer and cannot be spent, but they haven’t been transferred to your merchant account yet. This hold remains in place until you finalize the transaction or the hold expires. If no action is taken, the funds are released back to the cardholder after a set period, typically 5 to 7 days. Holds are often used for delayed charges, pre-orders, or services billed after completion.

If you don’t capture a transaction promptly, you risk losing access to those funds or sustaining a chargeback. And if you tie up a cardholder’s funds for too long, they could understandably get upset.

Understanding and managing authorization holds is an important but often confusing part of payment processing — especially for industries like hospitality, rentals, and subscription trials. If you obtain your merchant account from AltoPay, our team will help you accurately collect what you’re owed without introducing compliance issues or disputes.

A deep dive into authorization holds

Authorization holds can help your business optimise revenue. But manage them incorrectly and authorization holds can do more harm than good.

Let’s take a look at what authorization holds are, how they work, and if they’d be a good fit for your business.

How do authorization holds work?

Debit and credit card authorization holds temporary freeze money or credit in a cardholder’s account. They help ensure you, the merchant, get paid for purchases by preventing the cardholder from spending the promised money somewhere else.

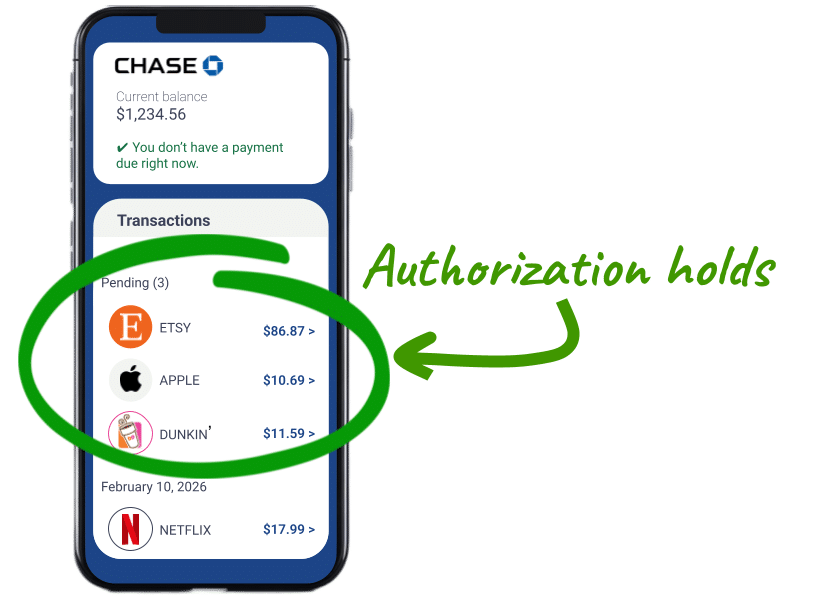

As a cardholder yourself, you are probably familiar with authorization holds. Holds appear on your credit or bank statement as a pending transaction.

Processing a debit or credit card transaction isn’t an instantaneous process. In fact, several days can pass from the time the purchase is initiated until the funds are deposited into your merchant account.

Authorization holds can help ensure the money does, in fact, make it to your account.

Here’s how an authorization hold fits into payment processing.

How long does an authorization hold last?

Timelines for authorization holds on credit cards and debit cards can vary.

The card brands try to balance the amount of time it takes you to settle a transaction with the amount of time a cardholder is willing to have their money or credit limits tied up.

There are several factors that can influence how long an authorization hold lasts.

- The card brand (Mastercard, Visa, American Express, Discover, etc.)

- Your merchant category code (MCC)

- The card type (credit or debit)

- The billing model (single sale or recurring transaction)

- The transaction type (card-present or card-not-present)

- The goods or services that were purchased

Here’s a high-level overview provided by Visa.

- 5 days — Merchant-initiated transactions (recurring transactions, installment billing, etc.)

- 5 days — Card-present transactions

- 10 days — Card-not-present transactions

- 10 days — Transactions with merchants with rental-related MCCs (bicycles, boats, costumes, equipment, furniture, etc.)

- 30 days — Transactions with merchants with lodging, vehicle rental, and cruise line MCCs

If a transaction is not settled within the given time frame, it should be cancelled.

PROS

Why should you use authorization holds?

Authorization holds can benefit your business in several ways. Here are a couple of the most common reasons why you might want to incorporate authorization holds into your payment processing workflow.

Holds can reduce revenue loss.

Authorization holds freeze the cardholder’s funds, ensuring the money or credit is still available when you settle the transaction. By preventing the cardholder from spending the money somewhere else, fewer transactions will be canceled and you’ll earn more revenue.

Holds can make sure you are paid the full transaction amount.

Depending on your industry, you might not know the final purchase amount when the transaction is initiated. Consider these examples.

- Hotel guests might stay another night or order room service.

- Rentals (cars, bikes, construction equipment, etc.) might be returned late or damaged.

- Online grocery orders might include items that need to be weighed before a price can be determined.

- Waitresses and bartenders might receive tips.

- Parking lots don’t always know in advance how long customers will leave their vehicles.

If you operate in one of these industries — where you provide goods or services before the final transaction amount is calculated — the card brands allow you to submit authorization requests with an estimated purchase amount. Then, you can set authorization holds for the anticipated amount and freeze the funds just in case they are needed. This helps ensure you can collect both the expected and unexpected costs.

Holds can reduce processing fees.

Payment processing involves different fees paid to different entities at different points in the transaction lifecycle.

Some fees are paid only if the transaction is settled. So if you never settle the transaction, you never pay the fees. And authorization holds can help ensure you only settle — and pay for — the right transactions.

For example, a customer orders a pair of shoes. When your fulfilment team goes to ship the order, they discover the inventory count was inaccurate — you don’t actually have those shoes in stock. If you use authorization holds, you can cancel the transaction and save the settlement fees.

Or maybe you receive an order and quickly discover it was made by a fraudster. If you have only put a hold on the account and haven’t settled it yet, you can cancel the transaction and save the corresponding processing fees.

Holds can lower your dependence on refunds.

Sometimes customers have buyers repose or otherwise want to cancel their transactions.

If you have set a hold, you can simply release the hold and the transaction will be cancelled. But if you have already settled the transaction, your only option is to issue a refund.

Refunds can have consequences. First, they often come with a fee. Second, if your refund count becomes excessive, your acquirer or processor will probably notice — and question your business’s reputation.

Holds can prevent chargebacks.

Setting an authorization hold is like pushing pause on a process that can become unnecessarily rushed. Holds buy you and your customer some time, allowing you both to review the situation and make sure you want to proceed.

Check these hypothetical situations and see how holds can impact chargebacks.

- You notice two orders, both from Rory for the same book. You email Rory to ask about the purchases. Rory tells you she didn’t receive a confirmation message after placing the first order. Thinking it didn’t go through, she tried again. Because you put a hold on the transaction, you simply have to reverse the hold to avoid a ‘duplicate processing’ chargeback.

- Luke checks his statement and sees a pending transaction with your business that he didn’t authorize. He calls you to report the suspected fraud. You reverse the hold and avoid a ‘no cardholder authorization’ chargeback.

- Patty signs up for a monthly subscription with your business. Moments after checking out, Patty realized she grabbed the corporate card by mistake! She can’t make a personal purchase on the company card! She calls you immediately. You reverse the hold and avoid a ‘cancelled recurring transaction’ chargeback.

CONS

Why shouldn’t you use authorization holds?

There are several benefits of authorization holds. But there are some drawbacks too. Make sure you understand both before updating your payment processing workflow.

Data has to be consistent.

All holds will eventually drop off the cardholder’s account — either because you settled the transaction or canceled the hold.

In order to do either task — cancel or settle the transaction — the issuer has to be able to match the hold with the settlement or reversal request. So you need to make sure you are passing the same information in both communications.

However, that doesn’t always happen.

Visa conducted a study on authorization holds. And this is what they discovered.

“Many merchants were sending incomplete or incorrect information in the authorization reversal message…Because of the missing or non-matching data elements, issuers were not able to match the reversal request to the original authorization.“

If you don’t provide the right information, you could cause the authorization hold to last an extra eight days — which could, understandably, frustrate the cardholder.

Hold amounts can cause confusion.

Depending on your industry, the card brands might let you set holds based on an estimated transaction amount. These holds — called pre-authorizations, undefined authorizations, or estimate authorizations — can cause confusion.

For example, a waiter sends an authorization request — with a hold — for 20% more than the final bill in case the customer adds a tip. However, the customer decides to leave cash instead of adding a tip to the credit card bill. Seeing the amount on his statement, the customer thinks he’s been charged too much.

This confusion can lead to frustration and possibly chargebacks.

Mistakes could increase costs.

If you put a hold on a cardholder’s account, you must act on it. You can set a hold and forget about it. You either need to settle the transaction or reverse the hold. If you don’t, you could be penalized.

For example, Visa charges a ‘misuse of authorization system’ fee for every approved authorization that hasn’t been reversed or settled.

Need help managing authorization holds?

AltoPay is a full service merchant account provider. We help our merchants create an effective payment strategy and continuously optimize it for ROI. If you are using authorization holds, we can help make sure you are using them correctly. Reach out to our team today.