Acquiring banks and issuing banks serve different roles in the payment processing ecosystem. Each one has distinct goals and responsibilities that ensure transactions are processed safely and efficiently.

OVERVIEW

Issuing bank vs. acquiring bank

Let’s start with a very high-level overview of issuing banks (sometimes called issuers) and acquiring banks (sometimes called acquirers) that can help you remember who does what.

ISSUING BANK

ACQUIRING BANK

An issuer is a bank for cardholders. It issues payment cards.

An acquirer is a bank for merchants. It acquires funds.

ISSUING BANKS

An issuer is a bank for cardholders. It issues payment cards.

ACQUIRING BANKS

An acquirer is a bank for merchants. It acquires funds.

Issuing banks explained

An issuing bank is a member of a card network (Mastercard, Visa, etc.) and is the financial institution that acts as the intermediary for cardholders.

The roles of issuers in payment processing

Issuers are most well-known for issuing payment cards.

Payment cards are issued to qualified cardholders who are allowed to make purchases at businesses that have been authorized to accept debit and credit cards as a form of payment.

But in order for cards to be issued and purchases to be made, issuers have to complete dozens of nuanced tasks behind the scenes. Here are just some of the responsibilities of issuing banks.

- Conduct background checks as part of credit card and bank account applications

- Open accounts and issue corresponding debit or credit cards

- Issue monthly credit card and bank account statements

- Process monthly payments for credit card holders

- Maintain points and rewards programs

- Manage bank account deposits and overdrafts

- Approve or decline transactions via the authorization process

- Forward cardholder funds to acquiring banks

- Initiate the chargeback process

- Review chargeback responses and assign liability

- Maintain compliance with card network rules and regulations

Issuing bank examples

Issuing banks can be members of multiple networks. For example, a bank might offer Visa debit cards and Mastercard credit cards.

According to the October 2025 Nilson Report, these are the 10 largest issuers in the world. Six are located in the USA; four are in China.

- JPMorgan Chase

- American Express

- Citi

- Capital One

- Bank of America

- China Construction

- Discover

- China Merchants

- Agricultural Bank

- ICBC

Acquiring banks explained

An acquiring bank is a member of a card network and is the financial institution responsible for liaising with merchants.

The roles of acquirers in payment processing

Like issuers, acquirers play an important role in ensuring transactions are managed safely, efficiently, and in full compliance with card network rules.

Usually, acquirers are most well-known for providing merchant accounts which enable merchants to accept, process, and settle card payments. But within that broad description of responsibilities lie dozens of nuanced tasks. Here are some examples.

- Establish risk thresholds and standards for what merchant types will and won’t be accepted

- Deny or approve merchant account applications

- Create accounts and issue account credentials

- Enable merchants to accept and earn revenue from card payments

- Receive and forward authorization requests to issuing banks

- Submit transactions for settlement and credit merchant accounts

- Record merchant activity including deposits and withdrawals

- Receive chargeback notices and debit merchant accounts

- Receive, review, and forward chargeback responses to issuing banks

Acquiring bank examples

Acquirers are often members of multiple networks, enabling merchants to process payments from all major card brands with a single merchant account.

According to the October 2025 Nilson Report, these are the eight largest acquirers in the world.

- JPMorgan Chase

- Worldpay

- Fiserv

- Global Payments

- Nexi Payments

- Adyen

- Worldline

- Getnet

How issuers and acquirers interact

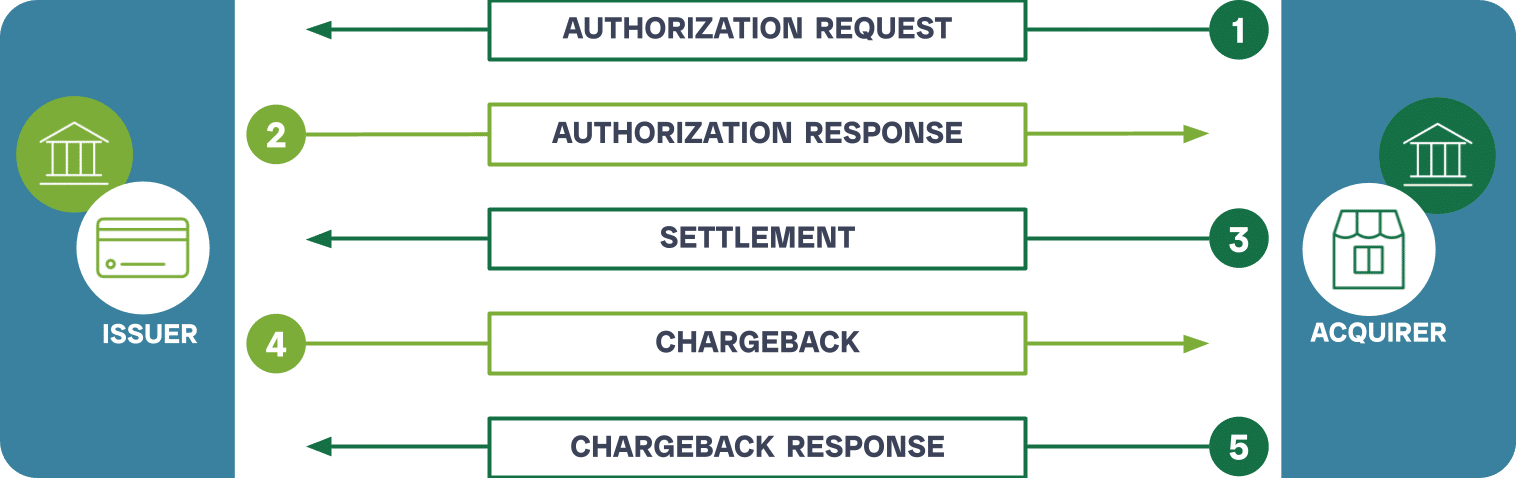

To illustrate how issuers and acquirers work together, let’s look at the complete transaction lifecycle.

Now, let’s look at a more detailed explanation.

NOTE

While the following provides more detail than the visual we shared above, it is not a complete overview. It omits entities like your gateway and CRM. The intention is to highlight the unique roles and responsibilities of issuers and acquirers.

If you’d like more information about the transaction lifecycle, feel free to reach out to our team with questions.

PHASE 1

Authorization request

A cardholder visits your site and adds a few products to the cart.

When the cardholder enters payment information and confirms the purchase, your acquiring bank submits an authorization request to the issuing bank.

The authorization request asks the issuer to confirm three things:

- The account is in good standing

- The account has enough funds or available credit to cover the transaction amount

- The card hasn’t been reported lost or stolen

PHASE 2

Authorization response

The issuer responds to your authorization request with a code. The authorization response code is a suggestion for how to proceed. There are dozens of response codes across the various card networks, but you will typically do one of two things:

- Approve the transaction.

- Decline the transaction.

PHASE 3

Settlement

Once a transaction is approved, it needs to be settled. Transaction settlement is the process of moving funds from the cardholder’s account with the issuing bank to your merchant account with an acquirer.

During this step, payment processing costs — such as interchange fees and scheme fees — are debited from the transaction amount.

Most card-not-present merchants have acquirers settle their authorized transactions in a single batch rather than settling transactions individually.

Settlement usually happens 1-3 days after the transaction is initiated, though some merchants might delay settlement. Here are a couple example reasons for delayed settlement.

- A furniture store authorizes a transaction immediately, but doesn’t settle the transaction until the sofa is ready to ship a few days later.

- A hotel delays settlements for several days to account for potential up-charges or fees incurred by the guest during their stay.

NOTE

Some acquirers choose to implement a funding delay. After the transaction is settled, the acquirer may hold funds for a certain number of days based on the risk factors associated with the account. Your merchant service agreement will likely outline if and when funding delays are used.

Once settled and funded, the transaction is complete — unless the cardholder decides to dispute it.

PHASE 4

Chargeback

In an ideal scenario, settlement would be the last step in the transaction lifecycle. However, the unfortunate reality is that not all customer experiences go the way we expect them to. Sometimes, chargebacks happen.

NOTE

The chargeback process varies by card network. The following is a general overview of responsibilities for issuers and acquirers.

There are additional phases of the dispute process that we don’t outline here — like pre-arbitration and arbitration. Those steps are network specific and can vary significantly from one case to the next.

If you have questions about what comes after the initial chargeback phases, feel free to reach out to our chargeback team.

A cardholder contacts the issuing bank to dispute a purchase. The issuer credits the cardholder’s account and forwards the chargeback notice to your acquiring bank. Your acquirer receives the notice and then takes funds from your merchant account to cover the chargeback expenses.

PHASE 5

Chargeback response

When a cardholder disputes a purchase, the issuer reviews the cardholder’s claims. In theory, only valid disputes are honored. But sometimes, invalid chargebacks slip through the cracks. For example, maybe the chargeback was submitted after the deadline or the cardholder was confused about the purchase.

If you think the chargeback is invalid, you can dispute it with a chargeback response. A chargeback response is a package of documents and information that support your case. The goal of a chargeback response is to prove the chargeback was not warranted or not compliant.

You’ll submit your chargeback response to your acquirer for review. If the acquirer considers the case legitimate, the bank will credit your merchant account and forward the response to the issuer.

The issuer will then review the chargeback response and decide if it’s a more compelling argument than the cardholder’s initial dispute.

If the issuer agrees with your argument, the cardholder’s account will be debited again and funds will be returned to your merchant account. If the issuer feels your response doesn’t adequately prove your case, the chargeback stands.

FAQ

Frequently asked questions about issuers and acquirers

Want to know more about how issuers and acquirers work together in the transaction process? Here are answers to commonly asked questions.

Are Mastercard and Visa issuers?

Visa and Mastercard are card networks, not issuers. Issuers are members of the card networks and issue cards on behalf of Visa and Mastercard.

Note: American Express and Discover complicate things! AmEx and Discover are card networks that also function as card issuers. Some financial institutions issue AmEx and Discover cards on the networks’ behalf. But these card networks are also equipped to issue cards directly to consumers themselves.

Can I process card payments without an acquirer?

No, you typically can’t process credit and debit card transactions without an acquirer. In nearly all situations, you would need to have a merchant account to accept card payments and only acquirers provide merchant accounts.

The acquiring banks’ relationship with card brands is what allows you to accept payments from cards issued by the network.

How do I choose an acquirer for my business?

Merchant accounts are possibly your most valuable business asset. You need to find an acquirer that can help keep your account safe and suits your business.

When looking for an acquirer, consider the following criteria.

- Card brands they work with

- Online reputation and reviews

- Available currencies and geographies

- Compatibility with your gateway, fraud tools, CRM, etc.

- Acceptable transaction volumes and maximum ticket amount

- Contractual obligations

- Customer support hours and channels

- Requirements for a reserve account

- Fees that come with an account (set-up, settlement, currency conversion, chargebacks, etc.)

If you are looking for a merchant account provider, we encourage you to consider AltoPay. Schedule a call with our team today to learn about the merchant accounts we provide.

Can I use a payment platform like Square, Stripe, Shopify, or PayPal as my acquirer?

Yes, you can use a platform like Square or Stripe as your acquirer. These are typically all-in-one merchant services and include everything you need to accept payments.

While these platforms may be convenient and easy to set up, they aren’t built to accommodate growing businesses. In fact, as businesses grow and face new challenges, their merchant accounts with these platforms are often terminated.

If you’re looking for stable, reliable payment processing, AltoPay can help. Schedule a call with our team to learn more.

If I have questions about my merchant account should I contact my acquirer first?

No, not usually. Even though the acquirer is your bank, you don’t typically work with the acquirer directly. Usually acquirers outsource customer service responsibilities to processors or ISOs.

If you have a question, reach out to the person who helped you set up the account.

Need help getting started with an acquirer?

Are you looking for an acquirer for your online business? AltoPay can help.

We work with growing businesses all over the world. We can provide a merchant account that is the perfect fit for your business, your industry, and your sales structure. Reach out today to get started.

AUTHOR

Jessica Velasco

For more than a decade, Jessica Velasco has been a thought leader in the payments industry. She aims to provide readers with valuable, easy-to-understand resources.